Q and A

KEFI Minerals is committed to providing full and transparent disclosure of its activities, primarily via releases to AIM's company announcement platform. KEFI also holds a live webinar shortly after the release of the Company's Quarterly Operations Report during which shareholders's questions are answered (and recordings are available on KEFI's website).

KEFI often receives follow-up questions as well as questions regarding how market developments may impact the Company. Under AIM rules, KEFI Minerals cannot be party to selective disclosure of information to individual investors. Whilst some conversations are about material already in the public domain, it is a Company policy to be cautious about one-to-one conversation with individual shareholders.

In order to make answers to these questions broadly available, KEFI has set up this Q&A page to post answers to questions which are deemed likely to be of general interest. If you choose to post these answers on a bulletin board, we ask you to publish the Q&A verbatim on the bulletin board and cite this page as the source.

Please email your questions to info@kefi-goldandcopper.com.

Q: You previously indicated a remaining funding requirement of $30m, including $20m via streaming and $10m via future equity at potentially higher prices. What specifically changed to increase the requirement to $46m, all via shares, and why was streaming no longer pursued?

A: The end of February arrived and KEFI felt it best to close the core financing package.

Having recently triggered the development schedule, timetable discipline is now imperative. The breakout of the Middle East conflict further prompted that we get on with it - not that it will be negative for gold over the longer term, but it simply reinforced the appropriateness of us closing our development funding.

In that context the parent company share issue provided an immediate route to locking down our fully funded position including extra for cost overrun reserves.

The banks and contractors were also keen to see this formally closed out. They are putting up 70% of the project development funding andare also listened to carefully and respectfully by the Board.

The share capital raised therefore reflects a decision to ensure the project is comprehensively funded, including appropriate contingency and working capital rather than continuing to rely on multiple yet-to-close conditional or sequential funding sources for the last pieces

Q: Why change plans against what was previously foreshadowed?

A: The Company would note that prior communications reflected at a particular point in time would represent its then-intention regarding the preferred funding mix. As is standard for any public company, such intentions are necessarily subject to changes deemed in the best interests of the company in response to external factors, including global events such as the extra risks introduced by the Middle East war, counterparty negotiations, and execution risk experienced in negotiations with different counterparties.

This should be distinguished from any notion of a fixed or unconditional commitment to stick to any particular funding route regardless of changing circumstances. The Board’s responsibility is to act in the best interests of KEFI shareholders based on the conditions prevailing at the time decisions need to be made.

Q: Why issue shares at such a discount to recent market prices?

We tried hard to defend the pricing and the price reflected weak general market trends since late February. Between 2 March and 19 March 2026, the industry index (Van Eck GDXJ) had dropped from 155 to 105 ie 32%. KEFI’s placing price was 31% below its share price on 2 March and a 14% discount to the closing price immediately prior to the announcement of the placing.

Q: Why have you not brought on a real institutional broker?

A: Perhaps the questioner is unfamiliar with Stifel, the multinational institutional broking firm which managed the Placing.

Q: It seems like the share price was hit by forward selling by bucket shops selling into the market to take placing shares at a lower price.

A: The placing was strictly restricted to institutions and a handful of other long term shareholders. None would have breached insider trading restrictions.

The institutional offering was closed on Thursday night after two days of wall-crossing and then the retail offering was opened to close on the following Monday night.

Q: The PLC has injected additional equity into the Tulu Kapi project, yet its ownership percentage appears unchanged. Can you explain why additional capital does not translate into an increased economic interest in the project?

A: That is an incorrect interpretation. We simply report circa 83% pending finalisation of the final beneficial ownership. But the end-result equity position for KEFI will depend on the facts of what each shareholder had invested. It is not a function of any negotiation.

Sorry for any confusion. It will be around 83% depending upon thoseactual numbers and the exchange rates at the time of investment. It should be noted that the Government’s investment will take another year or more to crystalise, as they complete their works (for which they earn equity).

In addition, the value of the underlying asset is enhanced by this additional equity, through de-risking and progression toward production, which is expected to benefit KEFI shareholders.

Q: Why do any exploration now and not just wait until there is dividends from TKGM?

A: Thefunds raised are first and foremost for the Tulu Kapi development.

The portion of the fundraising available for exploration is small at this stage, and conditional upon not being needed for development. Allocation to exploration funds would allow initiation of certain high priority key projects including the Tulu Kapi underground mining planning, synergistic regional projects that fit with Tulu Kapi and could extend production life.

The Board therefore views a measured level of spend for initiating exploration is a way to protect and enhance long-term value of Tulu Kapi and KEFI, not as a diversion from the core objective of bringing Tulu Kapi into production. To wait over 3 years for business-critical exploration is not preferred by the Board.

Q: What is the dilutionary impact on the value per share of this Placing?

A: From a percentage perspective, existing shareholders who did not participate in the placing will see their ownership interest reduced accordingly – about 20% of the post-issue fully-diluted shareholdings.

Importantly, the proceeds of the placing are intended to fully fund the development of Tulu Kapi through to production, which is expected to defend and materially increase the underlying value of the Company. As such, while there is near-term dilution in ownership, the objective is to defend and deliver a proportionately greater increase in asset value and future cash flow, thereby enhancing value on a per-share basis over time.

In summary, the placing is dilutive in the short term, but it protects the company and is expected to be value-accretive over the medium to long term as the project is de-risked and moves into production. Other equity instruments, such as royalties, obviously also impose their own form of dilution which we also analyse carefully.

Q: To what extent are Board fees, nomad fees, management salaries and bonuses absorbing the equity funds raised?

A: The capex budget includes all fees including commissions, bonuses and so on whether payable to banks, advisers, contractors, management or others. The aggregate of all of these costs is a small fraction of the total project costs which are borne by TKGM and funded from the project finance package.

The source of all the TKGM funding (including a cost-overrun reserve) will turn out to be approximately 65% bank loans, 5% Government investment, 5% royalty and 25% KEFI public shareholders. The attractive leverage provided for KEFI is reflected in the economic metrics of projected returns to shareholders.

Q: Various suggestions have been made regarding restructuring the Board, including recommendations of individuals that should have appointed in the past, and of which individuals should retire when, the levels of remuneration of the company’s leaders, when to pay whose bonus and so on. What is your response to on this type of advice and commentary?

A: The Board sees all submissions and takes full consideration of views volunteered by all shareholders. Also all Directors maintain dialogue with the major capital providers, partners, regulators and of course the industry-specialist advisers.

For shareholders’ information, the Board keeps its composition under review to ensure it has the appropriate balance of skills, experience, and independence to support the Company’s strategy. Each of the parent company’s independent non-executive directors was selected for specific industry expertise and track record. Each is expected to sit in on specific subsidiary boards and committees to ensure full transparency and effective governance oversight.

As the Company transitions from a development-stage business toward production, it is both appropriate and expected that the Board evolves accordingly. This may include the addition of further independent non-executive directors with relevant operational, financing, and jurisdictional experience, as well as ongoing succession planning and replacement at both Board and executive level. Strengthening independence and broadening expertise are key considerations as the Company enters a more execution-focused phase and looks to move to the Main Market of the London Stock Exchange.

All these matters are naturally being deliberated, will be reported as appropriate and remuneration details will continue to be regularly set out with benchmarking industry salary surveys referenced.

And as regards the suggestion that the Company’s Executive Chairman repay his 2025 bonus because the Company made this placing, that bonus was accrued upon satisfaction of its conditions, and for good order, with payment to follow this last piece of full finance being approved by shareholders.

A. We have consistently stated that, for security and privacy reasons, we rarely publish people’s photos - and only then with permission and after due consideration. This is an unprecedented huge financial impact project in an undeveloped part of the country. We treat our community with great sensitivity and respect.

Q: Why is mining contractor no longer investing equity?

A: It is good news that the mining contractor as it is still making the same investment but not receiving any equity share. That is a positive outcome of the retendering that we completed.

Q: Why not raise a simple traditional royalty instead of an equity-ranking royalty and why not complement it with a simple share issue?

A: A traditional royalty is much riskier in that the royalty provider gets paid before other stakeholders. Therefore it increases the risk of financial leverage.

As regards the suggestion to issue ordinary shares, we are striving to avoid unnecessary ownership dilution. We have been transparent that bank debt approvals in October allowed us to then focus on optimising equity structures and fully launching.

Q: Does KEFI have any licenses which contain critical metals, other than silver and copper?

A: We have opportunities and we do not discuss licensing strategy publicly

Q: Please comment on rumours of a possible takeover, partly due to public commentary by a journalist who claims to be close to management.

A: We do not know what has been said, have not discussed the topic with anyone and remain focused on building the business for its long-term returns.

Q: I have been investing in the junior mining sector for nearly 20 years and have been based in Saudi Arabia for the past seven years. This is one of the key reasons I have been closely following KEFI, as I share your view that the Kingdom offers very significant long-term potential for mining development.

While I am not familiar with the detailed terms of the Al Rashid agreement, I would encourage you to consider, where feasible, the possibility of applying independently for exploration and mining licences.

Given the evolving regulatory framework and the increasing number of opportunities being made available, this could potentially offer additional strategic flexibility.

A: All possibilities will be explored.

Q: Now that all the funding is effectively in place is Kefi able, even at this stage, to provide any forward guidance on a dividend policy? Feel free to caveat it as you think appropriate.

A: TKGM’s formal mandate is restricted to its licence area and, apart from servicing its business operational and reinvestment into that licence area, it targets to reduce debt quickly and pay out to royalty and share holders.

In turn, the KEFI group of companies above TKGM would place a priority on striking a good balance between reinvestment in business growth and dividends.

Feedback received from a long-term KEFI shareholder:

I have been invested since the Nyota days, but have regularly doubled up on major pullbacks, due to my respect for the effort you have been putting in. I've never lost as much on a stock, but fortunately this has paid off handsomely in the end, and I now have a substantial shareholding. Obviously I could have made much more buying the S&P500, but I should have lost almost everything given the problems that piled up, and am very grateful to you all for your miraculous efforts.

I have worked on the buy and sell side as well as investing personally for over 40 years. I cannot think of a company I have come across that has had to deal with what you have, and pulled through, and while you always deserved to come out the other side, few management teams would have kept the project afloat, and only a fraction of them would have done so with minimal dilution. Of all the stocks I have followed and owned, the journey and show of resilience has made this much more than me owning a "share" of a company, it feels much more personal.

I believe the compensation committee will recognize this, and I am supportive.

I hope the main drama has been in the exploration and funding, and not the mine development, but perhaps we are fated for a lively second Act, but regardless, I will sleep well - and salute your effort and success.

Thank you for pulling it off.

A: No, all remuneration as Executive Chairman (Chairman and CEO) is under one services agreement via his personal company Semarang as fully disclosed in the accounts along with other key PDMR remuneration. All remuneration (not just his) is set by reference to industry averages in independent reports.

Q. Now that the team has done a fantastic job to get Tulu Kapi to detailed documentation stage in very difficult circumstances, as a shareholder I personally suggest that post signing:

- Share consolidation. I think a ratio like 15 for 1 would make sense. It would bring the share price to say 30p, and it could go to 300p and still be a very manageable price. I think retail investors are put off by trading in the millions of shares, and it shows the issues which are now in the past. Much loved Greatland Gold is 662p now.

- Research note soon. Lord Ashbourne at Edison is well respected and knows the company and its history well. A note from someone like him with a full model would boost credibility, and confidence in forecasts. I think the AGM mid year for initial forecasts is too late for this.

- Ethopia boost event in London . Kefi should hold a drinks reception and short Tulu Kapi presentation at the Ethopian Embassy in Princes Gate, highlighting its close working relationship with the government, and raising UK institutional awareness. Even if they don't come they will see the invitation, and many will come I think.

- Online presentation on GMCO Saudi. My feel is the market values Saudi at close to zero. It would be great if the CEO and maybe the Artar family could join the presentation, and talk through their plans and aspirations. And also what sort of scale are the likely investments to take up, and how it will finance further project development. Their website was last updated in 2024.

- Online presence. The Kefi twitter account should have a post once a week with mine updates, and general developments in Ethopia and Saudi.

- Q and A on website. This is excellent and should be kept going.

A: Thanks very much for all your suggestions and we will endeavour to follow through as best we can on each of them.

Q: Can you elaborate about the Chairman’s succession planning? I am concerned to ensure that key relationships and knowledge is not lost.

A: Obviously financiers putting up development capital required commitment at the same time as plans to build up the team for the growth ahead. Nothing sensational in this. The Executive Chairman is indeed committed and the Company’s team building is natural for the next stage.

Q: Any comment on the Allied Gold takeover?

A: Ethiopia is Allied’s key asset and the takeover reinforces that Ethiopia is entering the world stage for the industry. The takeover pricing indicates that our valuation benchmarking errs on the side of conservatism.

Q: I suppose you are well aware that two unlisted royalty companies are promoting their intended investment in KEFI. Are they reliable?

A: There are more than two royalty companies negotiating with us and it is not appropriate for us to provide a running commentary in the public domain. The reliability of our counterparties will be established by their conduct before we announce the outcome.

Q: What would you say to the criticism that KEFI should have spent more on exploration in the past?

A: Exploration is indeed at the core of our strategy. Actioning on that front will come back to the fore again in the short term.

The past saw us diluting our GMCO shareholding in Saudi as the market did not support our exploration, and so it was sole-funded by the partner. And we already had sufficient resources and reserves to warrant development in Ethiopia. one could say that the cost of capital has driven expenditure.

Q: Does the company have recruitment, succession and contingency plans in place for the senior leadership people?

A: Detailed plans have been approved by our Board, partners and project financiers. They are an integral part of the project execution plans tabled and approved for the Tulu Kapi project financing syndicate.

Q: When can you set out detailed plans for the shareholders to ask informed questions about the looming production?

A: We will summarise our gold production plans in the Annual Report and look forward to discussing any aspect at the AGM, which are now planned to be held earlier each calendar year, as our reporting systems are being expanded for the next chapter.

Q: I am new to KEFI and would like to applaud your transparency. Few listed companies, have this Q and A service. I understand that you used to conduct live webinars for live questions. Can you please consider doing that again?

A: Thank you and of course we will consider your request with due consultation.

Q: Can the company do anything to ensure that bulletin board comment is by investors and not people trying to bully the company for their own self-interest, whatever it may be?

A: We can to close to nothing. And what is commonly referred to as Black PR may be annoying or distasteful but is commonplace across all industries.

- The total raised by placings this year for the purposes of finance closings and project launch represents less than 10% of funds raised in other forms from parties other than KEFI shareholders, who I am sure you can appreciate, also need to be seen to contribute – even if for relatively small sums. This is because of the long term commitments being made by Governments, multi-lateral banks, leading contractors, high-profile local investors and high-profile industry specialist investors.

- The placing price ascribes an entry valuation for KEFI of over US$200 million, which is several times that which applied at KEFI until recently and similar to that applicable to shares issued to the Government at the TKGM level. This will improve further as we make further progress.

- Given the commitments from lenders in October 2025, the equity package was assembled in December as announced and thus any remaining detailed documents are now being finished

- Lenders’ drawdowns commence mid-2026. But their detailed documentation is already circulating for wet signature exchanges. This sequencing of signings is typical for such transactions involving multi-lateral development institutions and many Government agencies. We are guided by our Project Finance advisers, Endeavour Financial who, along with legal counsel Herbert Smith Freehills, have closed scores of these multi-jurisdictional transactions over decades. Everyone is working diligently and collaboratively.

- The drawdown from the Project equity investors has started for some and for the rest is expected to start February 2026. Drawdowns are in accordance with a schedule to match spending with funding, especially spending vs funding in local currency, coordinated to minimize currency conversion risk for TKGM.

- Anything material must be via RNS; and

- The company website is not a publicity tool for unaccountable parties.

- GMCO resources are today over 3.5 million oz gold-equivalent, say double those of TKGM at 1.7M oz gold.

- GMCO will do its best to increase Resources within the licence to the south of Hawiah which doubles known strike length, and at Jibal Qutman where we have yet to test 75% of strike length.

- 83% of 1.7M oz resource at TKGM would be matched by 13% of 11 million oz Au-Eq in GMCO, which is 3 times current GMCO resources.

- These are not intentions or promises. But merely answering your question as to how might this be possible. Our record of discovery is exceptional as is the evidence of the exploration potential.

Q: Does the gold stream improve IRR to ordinary equity or does squeeze down returns to ordinary equity?

A: We carefully compared the choices assembled over a long period of time and optimised the mix between secured debt vs Ethio Prefs vs Equity-Ranking (subordinated) Gold Streams vs Ordinary Shares in TKGM vs Ordinary Shares in KME vs Ordinary Shares in KEFI.

The numbers set out in the announcement of 22 December 2025 report IRR to KEFI which is higher than the IRR estimated for any other financier at gold prices above c. $1500/ oz. Below c. $1500/oz the ordinary equity is squeezed down below the others who take priority.

After taking specialist advice, the Board concluded that we are doing well for shareholders in assembling choices and then optimising the selected mix. And more fundamentally, doing well to have assembled full financing as the first mover in the frontier market of Ethiopia for mining finance.

Q: I did not believe it was possible for KEFI to raise $340 million with barely any contribution from shareholders. Are you aware of anyone ever doing this before?

A: Not to this extent. we highlight that it is the robustness of the project that makes it possible.

Q: Do you agree that the funding package is complex and that it causes confusion amongst many shareholders, most of whom are inexperienced in what is being done to finance the development of Tulu Kapi?

A: The basic principles are simple and we certainly do our best to explain the key factors in the announcements and this Q and A, along with any additional details that a shareholder should need to know.

The debt and equity package is designed to optimise risk/reward and minimise overall ownership leakage.

Such large projects in frontier markets involve many stakeholders who need to be consulted and for whom risk-management is imperative on a multitude of fronts. This has all been well illustrated by the surprises and frustrations of our journey to get KEFI to this point. For example, this financing and launch has involved more than 100 legal advisers working for many man-years for more than a dozen parties.

The sense of excitement and relief that management feels and would like to do its best to fairly convey to shareholders is that the project is now:

- “positioned on a clear set of railway tracks”,

- led by a bespoke African-experienced implementation team on the ground,

- wrapped in a powerful experienced board of industry and country hands-on experts,

- complemented by a syndicate of key contributors with skin in the game (investors, banks and contractors), and

- taking off within the atmosphere of a boom-time in the sector and in the country.

The future will require no less tenacity that did the past, but it is refreshingly more controllable, enjoyable and rewarding.

We wish all shareholders a Merry Xmas

A: Africa hosts one quarter of the world’s 200 countries, is the highest growth continent, has a disproportionate share of known under-developed minerals deposits. Its countries present risks like every country does. Each one differs. As do regions within the countries.

We strongly advise that any investor deploy capital where risk is duly researched and considered acceptable to the individual.

A: KEFI has all these documents on our website.

Q: Do I understand correctly that KEFI has raised and spent about $100 million since its IPO 20 years ago, has a market cap of about $200 million is now raising over $300 million project finance debt and equity to retain 75% of a +$1 billion of net cash flow over the next 7 years assuming $3,000 gold?

A: That is a reasonable synopsis.

Q. Is this actually correct? Each US$10 million tranche is entitled to 3% of the gold produced from TKGM's mining licence until 30,000 oz of gold have been sold under the stream, after which the entitlement steps down to a right to buy 2% of the gold for the life of the mine. This gold is sold to streamers at 20% of prevailing market price.

So if you utilise the full $40 million the counterparty can purchase between 8% and 12% of gold for the life of the mine at 20% of market price?

That is like 12% dilution of the project!

A: The dilution impact is less than a share issue of that scale, but it is indeed dilutive in its own way. This is equity risk capital coming off the bottom of the cash flow after debt service. Therefore it is accordingly more expensive than a stream which ranks at the top of the cash waterfall. At the same time, it improves the IRR for shareholders. Ultimately, it is a matter of striking the best balance across the range of considerations.

Q. Congratulations on the progress made in light of the RNS shared today.

Further to the below, I note that there was no update on the expiry of the fixed lump sum costings. For clarity and to help answer my questions, in the Proactive investor interview dated 22nd October 2025, Kefi's executive chairman gave a thorough update, and stated:

"We triggered the design and construction contractor group called Lycopodium to set up the procurement because it’s a fixed price lump sum plant. And when you trigger them firming up the price you have to go within 60 days, that’s the deal, and that means around the end of November is the deadline... and we’re on a fuse now to launch”.

As I understand, the Lycopodium deadline has since passed. Given that changing costs present a moving target for finance completion, I believe that shareholders might benefit from understanding further clarity on whether:

Lycopodium construction costs remain fully fixed through to 31st of December; and what process would apply if they need to be renewed or re-certified?

A: The fixed costs have been locked in as a result of further negotiation.

A: We have been advised that it is no longer required for debt components. May be unnecessary altogether, subject to final dealings of the Tulu Kapi finance package.

Q: The Mining Licence expires in 2035. What then?

A: We have the right to renew for 10 years, twice.

Q: A small explorer claims to own the Tulu Kapi District Exploration Licences. Is this a problem?

A: It does not affect the next 10 years of production plans. Nevertheless we investigated and have just initiated administrative proceedings in respect of several third-party dealings in those Exploration Licences.

A: We have done this.

A: Depending on the complexity of the content, RNS announcements can take anywhere from one day to several to draft and clear for release, if no third parties are involved, i.e. just the Company and its NOMAD.

The involvement of third parties and their advisers can add more time and they will not typically start their work until the reportable event has occurred.

These are just generalised comments.

Please comment and provide breakdown of the pay rate and industry standards, not because I agree with him but I believe more transparency would perhaps help inform those who may otherwise be confused, such as new shareholders, especially institutional investors.

A: We do not comment on commentators. And we provide a generic response to your question without having seen the publicity you refer to. The pay rates of all personnel are set by reference to industry surveys tabled to KEFI's Remuneration Committee of Non-Executive Directors, with advice from independent experts. We provide the link below to the only published industry remuneration report we found on a public website is: https://home.bedfordgroup.com/mining_compensation_report-2023

As regards KEFI’s senior executive remuneration, we have transparently provided statistics previously and also specifically in respect of the founder and Executive Chairman via the statutory accounts and via this Q&A section of KEFI's website.

For ease of reference, the tenure and remuneration for the Executive Chairman is as follows: Mr Anagnostaras-Adams founded the company and has been its Chairman since 2006 (except for a couple of years). He took on executive duties and started being remunerated from 2013-14 as Chairman and Chief Executive since 2014. His average level of base remuneration for the dual role of Chairman and CEO is below the average for this role as set out in independent industry surveys of comparable companies/roles. Over the past 12 years he has was paid an average of £190,000 per annum in cash and £87,000 in shares. His STI and LTI arrangements are also set out in the financial reports and are well inside industry ranges.

Q: Does the Tulu Kapi finance plan include all the capital required to fund all capex, all fees and financing charges, all requirements to set aside contingency provisions and cash reserves and anything else payable?

A: Yes.

Q: Do the offshore banking arrangements provide full transparency of disclosures to the Ethiopian regulators including central bank?

A: Of course. How else would KEFI and all other project parties including Government agencies as contractor and shareholder plus multi-lateral development banks with Ethiopia as member country conceivably wish to operate! The question itself is strange to put it mildly.

Q: Do KEFI and the operating company TKGM get credit in Ethiopia for all past spending?

A: Yes, in all respects.

Q: Is the company aware of the “minimum market cap” thresholds of large investment institutions? And can you inform shareholders?

A: We do not know all institutions and all their rules. As a general guide, we believe that Tier 1 institutions would rarely consider investing in a company with sub-$100 million market cap and most would like companies to also plan for a main board listing. KEFI has above-average liquidity and above-average upside-leverage. So we think we are reasonably well positioned in respect of this matter as we now advance through our business milestones.

A: We are getting requests to break out all sorts of costs like insurance, financing, compensation to households and other matters.

We already provide pre-closing guidance of the net cash flow for shareholders and NPV at various gold prices. This is intended to cover all projected costs.

Post-closing we will also break out whatever confirmed detail is normally properly disclosed without breaching privacy or other rules.

Q. It was previously indicated that triggering the plant repricing in July would allow the plant capex budget to last just 30 days before expiring the fixed pricing of the plant procurement. Does this mean we missed the boat and had to restart and, if so, what did that cost us?

A: The refreshing of plant pricing was formally triggered following Parliamentary Ratification of AFC in May, is being finalised now and the planned closing timetable accommodates the procurement schedules.

Q: What happened to the contractor funding as part of equity?

A: It is a sub-set of the $10 million of equity reported in the RNS to be issued at post-closing prices, for fees and costs. This is an improvement on what we foreshadowed some months ago. We can only set out final details at closing.

Q: Has the company had difficulty arranging comprehensive insurance coverage including political risks? And what is the cost?

A: All insurances arranged, via Marsh McLennan - perhaps the world’s largest insurance adviser/ broker. All of these and other normal opex costs included within ASIC estimates as published.

Q: May UK retail investors invest in the Ethiopian subsidiaries?

A: That is not possible because KEFI’s Ethiopian subsidiaries are unlisted companies in which only qualified investors (as defined in Ethiopian corporate law and regulation) may participate via a Private Placing with large investment sums and, despite being minority shareholders, any participant must sign the respective shareholders agreements and pledge their shares to the secured project lenders.

Q: I am trying to understand why KEFI is targeted for criticism on the anonymous chat lines.

Has the company created enemies in its business dealings? Or would it likely be disappointed shareholders?

Your guess would be better than mine. any comments the company is able to make?

A: The sector was probably the worst stockmarket performer in the past 10-15 years.

Whilst KEFI was one of the minority on AIM that survived, and whilst it has been built to to a position that should generate excellent returns, undoubtedly any shareholder is justifiably disappointed by the share price historically. We suffered too many unforeseen setbacks and too much share dilution to suggest that anyone should not have been very disappointed.

That includes company leadership that was paid average industry salaries for what was riskier than average work, and in shares.

But management has not and will not complain. Board and management take it on the chin and all are very excited.

It is also true that we have created some enemies in business dealings, but never by doing anything other than using the force of law to protect KEFI. Most of these situations are confidential whilst a few surfaced in litigation which KEFI has always won.

Q: Some shareholders feel that Richard Robinson has been on the Board too long as an independent and that Alistair Clark is too close to the Chairman to be independent.

A: Richard himself requested some time ago that we expedite his replacement as he believes it is time for him to be replaced. The Board agrees with his assessment and candidates are being considered. However, we await the finalisation of various negotiations and consultations with the various stakeholders with whom we are presently finalising the Tulu Kapi financing. In regards to Alistair, his oversight on ESG is critical at this particular stage in Ethiopia , not just in management's opinion.

Discussion about the board composition is healthy - we appreciate feedback and reach out to consult people from various constituencies. Both Richard and Alistair are of the highest integrity and are certainly independent minded. They have known the executives for 5 or 6 years and neither could be described as a personal friend of any executive.

Q: Thank you for the detailed Q and A which is unusually transparent for a listed company. But how can future timetables be more reliable than in the past?

A: Upon signing the Tulu Kapi funding package, the syndicate of parties will have aligned on timetable and key milestones. Then KEFI will be solely responsible to manage to the agreed schedule rather than KEFI continuing to strive to assemble commitments from as yet uncommitted parties.

And this will have been made possible by a calmed-down working environment in Ethiopia.

Leadership style and management composition will then also need to adjust accordingly.Frankly, it will be a refreshing relief to the team to have formal contractual commitments from all parties to the agreed schedule as set out in an agreed project execution plan. and to wrap the process in the enlarged planned team will finally be both warranted and necessary.

Lastly , the plan this year has been to have documentation ready by end June for launch to trigger upon certifications being completed as soon as possible from that date. That is what is happening and we will obviously announce when that occurs.

- cash is raised at price x to repay liabilities; or

- shares are issued at the same price x to repay the liabilities.

- Mining package

- Construction package (covering on-site work, roads, and power)

- TKGM shareholders package

- Secured loan facilities package

- £300,000 annual entitlement to cash remuneration, of which £150,000 had been paid at y/e 24 and £150,000 deferred which has not yet been paid.

- Retention bonuses of £185,000 taken in locked-in shares and £238,000 deferred cash which is scheduled to be paid from the proceeds of Tulu Kapi project financing. These decisions were not his and focused on overall fairness. The arithmetic could have been done in several different ways.

- £10,000 cost of medical insurance.

- Proportion of the aggregate charged to operating joint ventures for 2024 was 75%.

- Mr Anagnostaras-Adams has been Chairman since 2006 (except for a couple of years) and also Chief Executive since 2014

- He has received total cash remuneration of average £190.000 p.a. over 12 years or £120,000 p.a. averaged over 19 years i.e. neither he nor KEFI’s then mother-company Atalaya received remuneration in the initial 7 years.

- These numbers assume that his remuneration is actually brought up to date at the finance closing of Tulu Kapi, as he is owed over 12 months backpay. He has asked to be paid last.

- He has received total shares (instead of cash) remuneration of average £87,000 p.a. averaged over 12 years or £58,000 p.a. averaged over 19 years because nil consideration was received in the first 7 years. The shares also helped align him with the outcomes experienced by shareholders. He has sold no shares

- Mr. Anagnostaras-Adams’ base level of remuneration of £300,000 p.a. for the dual role of Chairman and CEO was set by reference to the then average for CEO’s as set out in independent industry surveys of comparable companies/roles .

- The base level STI and LTI schemes are set out in the Annual Report in detail. The LTI scheme is refreshed annually by shareholders as regards the authority to issue Incentive Options.

- It is important to note that no Incentive Options are in issue to any executives, including Mr Anagnostaras-Adams, under the LTI scheme as it was felt appropriate to only issue Options after full funding of Tulu Kapi is closed and reported

- Most other mining companies then operating in Ethiopia declared force majeure and/or lost their licences. Mr Anagnostaras-Adams has taken no significant absence from the Company for very many years and the KEFI Remuneration Committee does not consider his compensation to be excessive in these most difficult period.

- It is the Board’s view that Mr Anagnostaras-Adams’ leadership and dedication, supported by the team on the ground with him throughout many threatening years, saved the Company - and we are now looking forward to launching a major project against a background of record gold prices. A very significant achievement.

- The aim of the company and Mr Anagnostaras is to wipe the slate clean after a very challenging and unrewarding chapter for KEFI, and to focus on the significant value-adding opportunities ahead for the long-term benefit of shareholders.

The main questions received recently are summarised below as often we have received several similar questions.

Q: Why have KEFI shares performed so poorly, and only just beginning to show any promise?

A: As objective as the company can be in answering the question:

- The mining sector generally has been out of favour for many years. KEFI hopes this is now changing given high gold prices. KEFI is among the small number of AIM junior miners that have endured over the past 15 years since the last gold boom (which peaked at a gold price of c. $1,900/oz). Since then, the majority AIM-listed mining and exploration companies have ceased to be listed. KEFI remains.

- Despite significant challenges in both jurisdictions, KEFI chose to continue advancing its projects. This included the necessity of negotiating significant regulatory reforms in both host countries. In Ethiopia, we had to safeguard the project from upheavals at all levels as the country introduced democratic reform, and unfortunately endured a civil war. In Saudi Arabia, permitting was effectively frozen for approximately 8 years. Conditions precedent for financing and launching had to be modified with changed circumstances in order to achieve “bankability”. Much of this was not foreseeable.

- As a result, a significant amount of time and resources were diverted to defensive and corrective measures rather than directly advancing project work. To sustain these efforts KEFI raised equity capital on multiple occasions. This was deemed to be unavoidable and a necessary action for survival under adverse conditions beyond KEFI's control. The alternative would have been to relinquish the projects; KEFI has not contemplated this. We have built a strong growth platform which provides potential value growth as the sector, our countries and our projects get moving.

- With the (then dilutive) raised funds, KEFI discovered or acquired gold-equivalent resources amounting to c. 5 million ounces, of which its beneficial interest is c.2 million ounces. All orebodies are yet to be closed off and a large pipeline of other opportunities is in place.

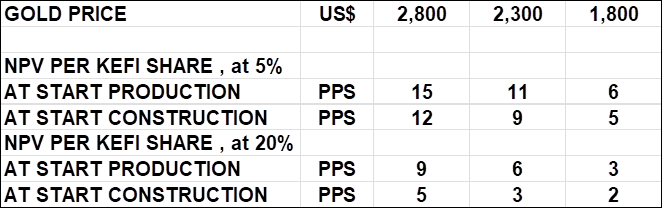

- Currently, the net present value (NPV) of the Tulu Kapi Gold Project attributable to KEFI, and based on US$3,000/oz gold is c. $900M or c. £700M. This does not include any valuation for KEFI’s 15% stake in Gold and Minerals Co. This indicates considerable potential valuation upside from the company’s current market capitalization of £53M (post the May 2025 capital raise) as KEFI continues to de-risk the Tulu Kapi Gold Project.

- There is further potential valuation upside from the Saudi assets. In November 2024, Orior Capital valued KEFI’s 15% stake in Gold and Minerals at US$50m to US$78m based on a comparison with recent M&A transactions in Africa. The report is available on KEFI’s website.

Q: When you quote valuations per share, why do you not build in further dilution for future share issues?

- KEFI publishes valuation-style information using industry conventional metrics based on actual share capital.

- Making assumptions about future share offerings would constitute Forward Looking Statements. This could be interpreted as policy, and could potentially be materially misleading. The Company on the other hand publishes its policy – which is to minimise dilution by optimising the structuring of equity-risk capital at the different levels of the corporate structure.

- KEFI also sponsors proper in-depth research, given the lack of such research from the broking community, which generally does not allocate the time or resources to that function unless they can justify it with commissions made on share issues. Such research usually builds in assumptions about future changes to capital structure.

- Recent in-depth research on KEFI is by Orior and Edison, both uploaded onto KEFI’s website.

Q: Why did you not sell 15% of GMCO instead of raising money?

- KEFI announced a strategic review of its 15% stake in Gold and Minerals Co on 13 November 2024. This was not intended to be a ‘fire sale’, but rather a thorough review of KEFI’s choices and the cost/benefit of sale vs the other alternatives being worked on.

- In that context, there have been several significant developments in respect of Ethiopia, as follows:

- BCM, a leading mining contractor, being announced as the Preferred Contractor for the Tulu Kapi project in April 2025. BCM has agreed to contribute capital to the project, thus reducing the amount of capital that has to be raised from other sources.

- Interest in the Ethiopian Preference Shares (one of the very few dollar-denominated instruments available in Ethiopia), and interest in KEFI’s critical minerals licences.

- Major institutions joining the KEFI register to strengthen the group’s parent.

- But there have also been several significant developments in respect of Saudi Arabia, as follows:

- Gold and Minerals being awarded the Umm Hijlan licence at Hawiah in January 2025. Your Board believes this additional licence area adds significant further upside potential to the Hawiah project, both in terms of the VMS structures, and with the substantial outcropping and mineralised Mamilah gold system. Selling the stake in Gold and Minerals quickly would have deprived investors of the potential upside from exploration and development of this highly-prospective and known mineralised area.

- The joint venture between Gold and Minerals and Hancock Prospecting being awarded the Al Hajar Northern exploration licence area in March 2025. Al Hajar lies on the Wadi Shwas Mineral Belt, a trend that is approximately 50km east of the Wadi Bidah Mineral Belt that hosts Hawiah. Al Hajar hosts known mineralisation, and historical work supports walk-up drill targets. There is the potential ultimately for Hawiah and any discoveries at Al Hajar to be developed jointly, with substantial potential synergies and cost savings. Again, a quick sale of KEFI’s 15% stake would have deprived investors of this further development potential.

- The placing timing was driven by year-end audit sign-offs on solvency at KEFI, combined with pressure from KEFI’s bankers, contractors and the Government to commit certain costs (much of which can be recouped in due course) before drawdown of project finance for Tulu Kapi.

Q: How is the relationship with the majority Saudi partner, in light of the strategic review so far?

- The relationship with our JV partner is excellent.

- GMCO is now looking at the development of Stage 1 at the Jibal Qutman Gold Project in the short term, to be followed by that of the Hawiah Copper and Gold Project. GMCO will also keep under review the possibility and optimal timing of a GMCO IPO. These are not imminent actions, but longer term possibilities.

- ARTAR’s is a conglomerate which has until this past month been completely private. And it is therefore interesting that its first IPO was implemented only this past week - for ARTAR’s medical group SMC, which has publicly reported that it raised $500M for c. 30% of that subsidiary and that the IPO was oversubscribed many times.

- It is notable Saudi stock market places an attractive valuation on the only listed private sector-controlled miner, AMAK, which implies a very high potential valuation for the comparatively larger GMCO when it is production.

Q: Why does KEFI need institutional shareholders?

- KEFI is proud of its large retail shareholder following, with share turnover of over 100% pa being a healthy thing for any listed company.

- However, the transition of KEFI from explorer to producer requires structural change at many levels, including to introduce institutional long-term shareholders, which will also add stability and support to the underlying share price. The sale of the GMCO shareholding, even if it had already been possible, would not have addressed this matter.

Q: Why did you need to raise money if capex was already covered “there or thereabouts” with funds already arranged or falling into place?

A: We tried hard to ensure the capital raise of Q4 2024 brought us to financial close, however the delay to achieving Ethiopian Parliamentary Ratification of our bank’s country membership reaching this point plus some costs being brought forward, meant we were required to raise funds. The rationale of the raise was therefore:

- protecting solvency; and

- respecting the requests by the lender syndicate which, after all, is putting up almost all capex funding.

The bottom line is that the Project needed the money and KEFI had to put it up. We were fortunate that we were able to raise a large portion of the funds with specialist gold and other institutional investors, which concurrently addressed another important structural issue. Despite the additional shares in issue, the potential underlying value of KEFI continued to grow at the same time as the shares on issue and therefore remains many multiples of the prevailing share price; having taken so long to get the Tulu Kapi Project to a position of financial close on the broader $320M syndicate, we had to protect the Company’s position and did not want to delay or put the closing at risk.

Q: What was the basis for pricing the placing?

A: The KEFI share price has been at or below the placing price for practically the whole of 2025. Indeed on 1 May it was still below 0.55p. The uptick in share price stemmed primarily from a tweet from the Ethiopian Government (not KEFI) that it was set to finally award AFC its long-awaited country membership, which it subsequently delivered upon. Whilst this led to an improved share price it was also a contributing factor requiring KEFI to undertake a placing for reasons previously outlined. Given the historic share price during 2025, the placing price reflects very favourably to 20-day VWAP and beyond, whilst also being at the same level as the Q4 2024 raise.

Q: How do you explain the share turnover of +500M shares on the day the placing was announced?

A: 420M was the booking of one of the specialist gold funds that subscribed in the placing for £2,310,000. As announced, the shares from the Placing are to be admitted on 28 May 2025, at which point they would become a circa 4.5% owner in the Company. As a discretionary investment manager, a TR1 is not required to be filed by the specialist gold fund until its shareholding increases above 5%.

Q: Who are the institutional shareholders?

A: We now have quite a few institutional shareholders , mostly on-boarded over the past 9 months. It should be noted that no shareholder needs to publicly identify itself until it owns 3%. The institutions who permitted us to disclose their involvement herein are Ruffer Gold Fund, RAB Capital, Konwave Gold Equity Fund and Premier Miton. Time did not permit more of the other institutions to respond in time for this publication.

Q: Explain again the make-up of the funding package and the role played by the funds from the recent placing:

- The standing budget is $320M (currently undergoing final refreshing ahead of close) after deducting the mining fleet to be funded by the mining contractor and recouped from opex charges.

- Assuming the capex budget remains $320M, the funding sources are targeted as follows:

- $240M Secured lenders (committed by specialist African banks TDB and AFC)

- $80M equity-risk capital:

- $20M government, committed

- $23M mining contractor, committed in-principle

- $22M non-convertible Preference Shares issued by KEFI Minerals Ethiopia, commitments in-principle

- $15M already spent or already catered for in recent placing

- The above-listed aggregate is $80M, with some further flexibility within some of the components

- A small percentage movement (up or down) on the budgeted capex number can impact the final requirement. That is normal project management and is why we currently retain some flexibility within the syndicate allocations.

- We will also need to ensure that the disbursement schedule matches the FX drawdown schedule, either by domestic FX conversions or synchronising the currency of the drawdown.

- These matters are as finalised as they can presently be, pending the completion of the current exercises of confirming final budget on the eve of signing definitive documentation. Much of these exercises could only be triggered upon receipt of Parliamentary Ratification. To have jumped the gun would have risked having to duplicate the finalisation of certain costs.

- The total contracting package for capex and opex at Tulu Kapi represents aggregate financial commitments of almost $1 billion. Various teams on the ground and in the relevant international locations are well aware of the need to manage the process tightly and quickly. KEFI is responsible to lead, coordinate and support the overall process. In doing so, it has a fiduciary duty to its shareholders and also to its partners and its other financiers to strike an appropriate overall balance.

- There has to be “give and take” between the different stakeholders which is sometimes challenging but normal for such a large project.

Q: Please elaborate on the possibility of $5M costs being paid by KEFI shares, which has been referred to in recent investor presentations. Does that include any amounts payable to PDMR’s? Do any individuals have conflicts of interest?

- There are potential success fees payable to non-PDMR’s which exceed $5M.

- A smaller amount of potential bonuses also exist to PDMR’s (these have already been disclosed in past announcements and the Annual Report).

- It is reasonable to assume that an aggregate of a total of $5M of these fees will be accepted in shares if that is what KEFI wants/offers.

- The pricing of any of these shares would be at prevailing market prices post financial close (expected by the Company to be materially higher than current levels).

- They can also be paid in cash (assuming KEFI has the cash resources).

- This is a small fraction of the total project finance budget and provides flexibility in planning.

- The Company deals with conflicts of interest daily. It is part of fiduciary management to identify such issues and behave compliantly and honourably in all respects. KEFI’s assembly and preservation of alliances with Governments and major in-country and international organisations at all levels of the organisation should give some comfort to those stakeholders who are unfamiliar.

Q: How will we fund the KEFI corporate costs during construction at Tulu Kapi?

- Until any explorer has started production, all funding must naturally come from equity or debt. Plus in our situation, some past KEFI costs may be refunded in cash rather than converted into equity in projects

- Future corporate costs will remain under £1M per annum, bearing in mind the low-cost base in Cyprus and also after recoveries of costs from operating subsidiaries. KEFI has a contractual obligation to its financiers and contractors to build, oversee and support the fledgling project organisations, and we charge full refund of associated costs accordingly.

Q: How are salaries set - they seem so much higher than average income in the UK. Please specifically refer specific details with respect to the Executive Chairman, Finance Director and Chief Operating Officer.

- KEFI pays industry standard salary based on independent mining industry surveys, which has nothing to do with UK average incomes. And it is absolutely critical to recruit internationally experienced expert management for the first production project, let alone seriously pursue the company’s ambitious growth plans

- The remuneration of the top 3 executives is detailed in the Annual Report. Others in the group have been paid more than them but, to demonstrate commitment to the team, all three have typically historically taken their salaries twelve months in arrears and a large portion in shares, to support KEFI and align with shareholders. PDMR’s would make a formal disclosure if these shares are ever sold.

- Role definitions, performance reviews and remuneration decisions of these three and of all other personnel, are carried out by the Remuneration Committee and its sub-committees which take independent advice. We have a formal industry standard system, tying incentives to the specific KPI’s for which the executive is responsible.

Q: What is the history of the Executive Chairman at Atalaya Mining in Spain, KEFI and Venus Copper in Cyprus?

- He personally founded the three companies in 2005, focusing the combined missions of the three fledgling organisations on the Tethyan Belt from Spain to Cyprus, into Turkey and down into the Arabian Nubian Shield

- He stood down at Atalaya in 2013 to facilitate Spanish management once that company and its project was set up. It had hitherto been a mess but was then ready for localisation, which is critically important in southern Spain. He had no further involvement other than to support Atalaya and the Spanish authorities in prosecuting certain interfering third parties.

- He then switched his executive time to KEFI, which needed to achieve permitting, financing as well as to develop and not just remain focused on exploration. This was at the invitation of the major shareholders of the company which then owned Tulu Kapi Gold Project, which KEFI then proceeded to takeover and put in the right direction for development.

- Atalaya later transferred Venus Minerals back to the Chairman as Atalaya was uncommitted to Cyprus. The Chairman installed a team and JV partner to manage that whilst he has focused intensely on KEFI.

Q: When is the Annual Report being issued and when and where is the AGM being held?

- In early June we will issue the Annual Report, to be followed by a webinar with Q&A say a week later, to be followed by an AGM in London, which will have to be in July. We adjusted our plans last week in response to shareholder requests.

- We have had most AGM’s in London, but we have held it in Cyprus and Addis Ababa the last two meetings given attendance/cost. In response to recent requests by UK shareholders we are now arranging to return it to London this year and we will refine as shareholders wish.

Q: There was publicity about an EGM being proposed. Is this correct?

A: No formal request has been received. But we will be pleased to steer enquiries as appropriate.

Q. Is KEFI concerned that they have misled the market and their shareholders in that the timelines and information which has been released over the past 6 months was known to be false and / or unachievable?

A. Our announcements always provide achievable timelines that are always based on having checked with the counterparties involved ie they are reliable estimates at the time of publication if everyone delivers on schedule. However, the nature of such forecasts is that we can’t factor in potential delays from factors outside of our control. The main culprit recently was the delay in Ethiopian Parliamentary ratification of AFC Country Membership.

Q: Why be some open with communications if predictions of other people’s actions are often proven wrong?

A: That fundamental challenge will diminish as Tulu Kapi is launched and its progress much more predictable, with the funding under KEFI’s control rather than the control of other parties.

Q. Can the company please detail what they have spent over £1million per month on since the December raise?

A. The previous raise was mostly to repay liabilities as reported at the time.

Q. How can KEFI justify allowing Edison to release information on 20th March 2025 stating "No More Equity at Parent Company Level" and that short term funding is available at this stage of financial sign off if this is false?

A. Key events that have happened since publication of the Edison report are the delayed timing of Parliamentary Ratification and the fresh demands of the banks for closing and commitment fees.

Q. Why do we never hear from Eddy Solbrandt? Is he even really “employed” at this point?

A. As KEFI’s COO, Eddy is focussed on managing most of the Company’s employees and in particular the work being done to prepare Tulu Kapi for development. KEFI’s Executive Chairman is focussed on all “external relations”. This split of responsibilities is normal appropriate. Eddy will likely be at at least some of events in London that we have undertaken to host if anyone wishes to meet him.

Q: What if shareholders want more interaction and communication with the Company?

- KEFI considers itself more transparent than most, without breaching regulations or commercial-in-confidence matters. We try to be very communicative, such as with this Q&A.

- We also until recently maintained Quarterly Reports and Webinars, neither of which is a regulatory requirement. We are happy to re-activate those processes if that is preferred by shareholders and will take another poll at the Webinar we will now hold in June to ensure this is a broad-based request.

- One thing we cannot do is to provide exclusive briefings to selected shareholders or subsets of shareholders, in particular unregulated shareholders. We used to have shareholder get-togethers several times a year and that can also be re-instigated if numbers justify but the invitation has to go to all shareholders.

- The Board itself is structured to seek maximum alignment with the business agenda and with shareholders’ wishes, as follows:

- a deliberate balance of the spectrum of key mining and in-country expertise. This can be seen in the individuals’ CV’s as set out in presentations and the Annual Report.

- We have analogous structures at subsidiary boards.

- A majority of independent non-executive directors at the parent company board.

- An overall composition of the parent company board which is reviewed and renewed annually by shareholders, with 2 directors standing always down each year for review and re-election at the discretion of shareholder vote.

Q: Are the consultants' success fees mentioned on Slide 12 of KEFI's May presentation included in the disclosed options/warrants?

A: KEFI has negotiated the right to pay some service providers in stock at market prices post signing. Not an obligation. We will optimise in the final allocations.

Q: The metrics on TK Project Economics slide have changed between February and May KEFI presentations. Why does the May scenario have fewer tonnes at lower grade & throughput?

A: The open pit numbers are unchanged and the preliminary economic assessment of underground was refined. Immaterial impact on the overall value proposition and we will provide detailed updates in the Annual Report to be released soon.

Q. I note in your latest presentation you mention the following:

Final Board Ratification by banks upon Parliamentary ratification of AFC Membership.

As per your RNS dated the 18th March, you said , “the Company has now been advised that both banks have also processed Board approvals for the Tulu Kapi project”.

Once conditions have been satisfied it is my understanding that no further approvals or ratification are required as per their process:

When the Africa Finance Corporation (AFC) grants a conditional board approval for a project or financing arrangement, this approval is typically contingent upon the fulfillment of specified conditions. Once these conditions are satisfactorily met, final board approval is generally not required. Instead, the process advances to the next stages, such as legal documentation and fund disbursement.

Understanding Conditional Board Approval

A conditional board approval indicates that the AFC Board has agreed in principle to support a project, subject to certain prerequisites. These conditions may include:

- Completion of detailed due diligence

- Finalization of legal agreements

- Securing co-financing or guarantees

- Obtaining regulatory or governmental approvals(Green Climate Fund)

Once these conditions are fulfilled, the project can proceed without necessitating a second round of board approval.

Post-Approval Process

After meeting the stipulated conditions, AFC typically moves forward with:

- Drafting and signing legal agreements

- Disbursing funds according to the agreed schedule

- Monitoring project implementation and compliance

This streamlined approach allows AFC to efficiently manage project timelines while ensuring that all critical requirements are addressed.

For specific details regarding a particular project's approval status or conditions, it's advisable to consult directly with AFC or refer to official project documentation.

Thus, I am confused as to why it needs final board ratification. Can you please clarify.

A: Your analysis is correct, as regards AFC. AFC Board has indeed approved. TDB has also approved but needs to ratify the expanded facility.

A: As regards the works on the Mining Licence area: the Owner’s team designs the mine, process flow-sheet and on-site infrastructure. It takes specialist advice as and where required.

The plant and site infrastructure flow-sheet is then optimised, detail-engineered and its building overseen by Lycopodium. Lyco is a process engineering contractor.

The earthmoving for infrastructure is by the civil contractors under Lycopodium and for the mine is under the mining services contractor, BCM. BCM is a civils and mining contractor.

Both Lycopodium and BCM report into TKGM Project Management , all monitored overseen by KEFI management. KEFI Non-Executive Directors also sit on operating company Boards, as do partners’ representatives. KEFI controls overall and warrants to protect the contractors, partners and financiers.

Q: What happened to the previous mining contractor?

A: They were replaced for the reasons given in the RNS.

Q: Did the change of mining contractor impact Lycopodium or other contractors?

A: No

Q: Why did you not flag the possible change of mining contractor?

A: It was commercially confidential and in the Company’s best interests to keep it that way.

Q: Shareholders did not see coming that a new mining contractor would contribute to the TK funding syndicate. Are there more surprises coming?

A: We have always said we would optimise the finance plan and we will keep doing our best to maximise choices and negotiate best outcomes.

Q. The TK funding requirement of $320m is now serviced by reported commitments from the Federal Government ($20m equity in the JV company), the 2 banks ($240m in senior and subordinated debt) and the newly appointed Operator ($23m). That leaves $37m unaccounted for although our money has been relentlessly ploughed into the project and may have discharged that proportion of the budget already. Can you clarify this?

A: As regards your use of the term ”Operator", this conveys a fundamental misusnderstanding which deserves explanation. The Operator is the Owner, TKGM. The Guarantor of the Operator’s performance is KEFI which has undertaken contractually to provide the human and capital resources for TKGM to perform. That is because KEFI is accepted by the contractors and banks to develop TKGM into the organization it needs to become. Partes like Lycopodium and BCM (newly appointed mining contractor) are contractors to TKGM.

As regards your “unaccounted” $37 million, we do not really understand the question. EthioPrefs remain part of the plan and will provide the largest contribution to this portion, supplemented by capex already spent and any last-minute tweaks amongst syndicate members if and as required once final costings are certified.

We maintain the Company’s focus on maximizing non-dilutive capital-raisings wherever reasonable to do so. This is succeeding with the contractor financings, debt capital, the TKGM share capital and the Equity Risk Notes to BCM and planned Ethiopreference Share investors. Accordingly we feel thatwe have removed any concern about whether the finance will close successfully.

Q. Has the process for refreshing the contractors contract already started? If so, is it wise to spend 500k doing this (Harry's quote on the vox interview) before ratification has even been granted. If it isn’t being refreshed now and it takes 2 months to complete (Harry's timeline in the same interview) how are we going to be in such a position to (in Harry's words) "look at each other in June" and start construction when this piece of work will still need to be done?

A: We agree that ratification needs to be clarified and we note that is reportedly imminent. The Lycopodium price-refresh then takes one month to yield results good enough to finalise negotiations. Certification and signing will take a little longer.

Q. It seems with every update that resettlement of the community is being prepared. Yet preparations never seem to be completed?

A. That has not surprised anyone experienced in moving a community of 1000’s of people, besides it being the first project of this nature in Ethiopia. The government has recently completed property surveys for Phase 1 of the resettlement which is the piece on the critical path at commencement of Major Works.

Q. Harry mentioned that physicals such as starting the build of construction camp, drilling of water wells ETC will now be sequenced to start over the next 2 months. Can this be elaborated on?

A. Current activities include a new security camp now being built adjacent to mining licence area, expanded water source installed. These are expansions of facilities as the numbers of people involved is increasing.

Q. The RNS dated 13 November clearly laid out the reasoning for the GMCO Strategic Review and sale of the Saudi assets. This included prioritising its majority owned projects, focusing on a large Ethiopian pipeline and that raising sufficient funds for Saudi is considered too dilutive. How has the potential $23m injection into Tulu Kapi's pre-production costs changed the reasoning of the above?

A: We believe the combination of the Ethiopian Preference Share and the partnership with BCM will negate any pressure to dispose of our stake in GMCO in order to fund Tulu Kapi. And while we remain firmly focused on majority owned projects we also believe that there is tremendous value in the GMCO business.

Q. Why has the remaining TK capex reduced by $20m to $300m?

A. The $300m figure that you refer to is net of contractors’ funding contribution and thus excludes the $20m investment by the Ethiopian Government.

Q. In the update of 7 January 2025, $60m of the required funding comes from up to $30m Ethioprefs and $30m from ‘certain Middle Eastern and other sectoral investors’. Can you please clarify what has happened to the interest of these Middle Eastern and sectoral investors as it appears that their investment is now to be replaced by the Saudi sale proceeds?

A. The following information hopefully provides clarification and background.

The total amount required is being reconfirmed for its last minute-fixed pricing elements. If we assume no change from $320M, $240M is planned from debt-capital and $80M equity-risk capital (including the Government's investment). Given that the debt component has settled down and is now being prepared for closing, we now naturally can optimise and finalise the equity capital from amongst the choices created over the years. We have done this quite deliberately so that KEFI is not over-reliant on one equity source or another.

Accordingly, KEFI still optimises capex contribution by contractors, contribution by Preference Shares issued to local qualified investors, specialist investors in the region focusing on our pipeline in either or both Ethiopia and Saudi Arabia and, of course, other parties with a declared interest in KEFI. We are not in a position to provide a running commentary on the amounts provided by the various equity investors until deals are done. There will be ebb and flow of the planned contribution from each investors and that is unavoidable until we have completed the process.

Further background on KEFI's approach to funding Tulu Kapi is available in this interview:

VOX Markets - Q&A with KEFI's Executive Chairman, Harry Anagnostaras-Adams.

Q: Can you also please comment on why KEFI did not provide reasons or explanations for timeline slippage in the RNS?

A: We assembled the debt offering and documents by the end of March. Before signing, we need to, with counterparties, finalise certifications, optimise equity and satisfy conditions precedent. Those things could not be done without having clarified the debt offering. These processes will take approximately 2-3 months and were explained in KEFI's most recent RNS.

Q. Is triggering Tulu Kapi's development now dependent on selling GMCO?

A. No.

Q. With AFC ratification a critical element to finalise financing, shareholders have been told that all parties are aligned, yet its completion date has continuously been pushed back and missed. Why should investors have confidence that Kefi can deliver on the most recent dates?

A. KEFI does not run the Ethiopian Parliament. But we have been advised by the highest Government officials that we can rely on that process being completed such that it will not in any way hold up the launch. That is the reality.

Q. The 8 April RNS notes that construction of initial site facilities is underway as well as expanded water supply and camps for construction and security. When will you provide photos of these site construction activities?

A. We are aware that there is some interest in seeing photos of site activities. We do plan to do so but need to judge when it is appropriate to publish photos of site activities based on privacy and security priorities.

Q. Why is there secrecy about the ratification process, I cannot understand why a timetable cannot be published?

A. Ratification is a parliamentary task, and we are advised in good faith that ratification is in process within project requirements. The company is in no position to dictate parliamentary timetables or advise on how long other agreements have taken to ratify. Today's RNS notes that the focus is to complete this quarter Government approvals of residual administrative matters, including AFC membership ratification by the Ethiopian Parliament.

Q. I note that the area surrounding TK and also to the North not only still belong to the Hong Kong shell company, but have recently been extended for another year. Can you please comment on what the company is doing in respect of this, and whether you still expect them to be “returned”?

A: We remain confident that the successful launch of Tulu Kapi will sort this issue and our administrative processes remain focused thereon. It is not in shareholders’ interests to elaborate publicly.

A. The Hancock RNS was released once the Saudi Government decided we had won the tender. And even it had been an application rather than a tender, we would need to await the granting of the licence.

Q: Why is it that Ethiopia appointed KEFI’s Chairman as consul to Cyprus?

A: The Ethiopian Ambassador to Cyprus also looks after 11 other countries and she wanted support on certain specific economic initiatives in Cyprus, such as targeting Cyprus Pharmaceutical companies to manufacture in Ethiopia for import replacement – just as important as export generation.

Pharmaceuticals is the largest export sector from Cyprus, exporting to over 120 countries from about 20 factories under a number of companies. The Chairman has successfully carried out those honorary duties during his brief stopovers in Cyprus.

Q: I read in the media that a civil war in Tigray has started again. Please comment.

A: The past “civil war” was a 5% ethnic minority attempting a coup and being squashed by the 95%. The Tigray Region is on Ethiopia's border with Eritrea and about 1,300km from Tulu Kapi.

In Tigray last week, one Tigrayan seized power from another and then headed to the federal capital to talk it through. That is what we saw on the ground.

Q: If the community wants the project to have gone ahead already, why have you not moved them already?

A: It would have been illegal without simultaneously triggering the Project and its programs for all those people.

Q. When will you hold your next webinar?

A. We have elevated our disclosure plans (and shareholders expectations’ in respect thereof) way beyond regulatory requirements. Anything other than an RNS is not required from a regulatory viewpoint and anything “extra” like a webinar or a website Q&A is sometimes impossible because the Company is “pregnant with about-to-be-disclosed material information”.

And, of course, if the company informed shareholders that it is pregnant with undisclosed material information, that of itself is an unclear disclosure which is unfair and unhelpful to shareholders. It sometimes takes weeks for multiple significant counterparties to approve a KEFI RNS.

So…frankly it has been a frustrating struggle recently to slot in a webinar due to the large number of milestones to report in recent months in particular. We like being transparent with the Q&A and with Webinars but that enthusiasm must be tempered by regulatory rules and guidelines.

We’ll time the next Webinar after taking advice from the NOMAD in particular. It may be necessary to change its format and, for instance, invite one of the independent research analysts to present their refreshed deep-dive report (after meeting senior in-country management) and filter questions on sensitive areas.

Be that as it may… the main thing is to make progress and report formally as soon as possible.